Construction AI in 2024 Part 2: Six Areas of Application

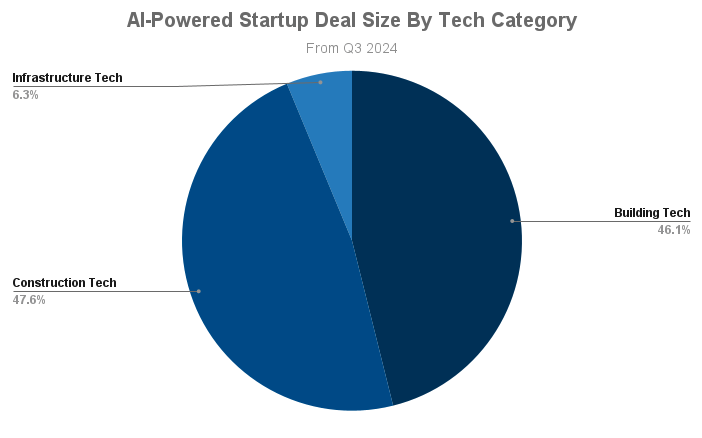

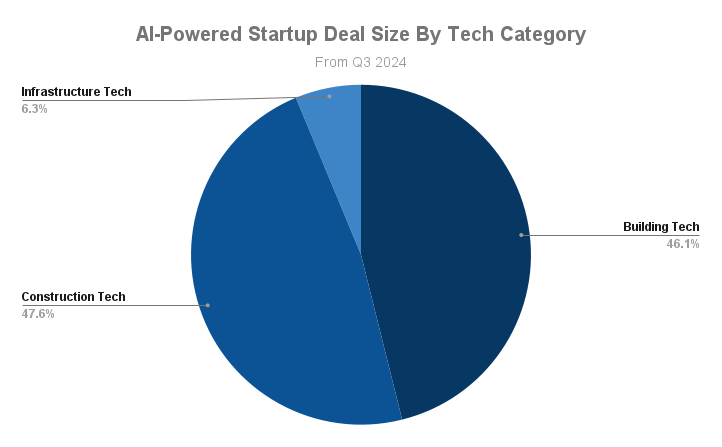

Source: https://builtworlds.com/wp-content/uploads/2024/10/AI-Powered-Startup-Deal-Size-By-Tech-Category.png

The companies outlined here are divided into six areas. There are thumbnail outlines of around 100 companies, ranging from large and recognised technology leaders to startups [1]. The divisions are not always neat, particularly for the larger systems because there are overlapping functions, and there are subsets within the six divisions. It does not attempt to cover every new company everywhere with a construction related AI system, but is a comprehensive if not complete survey of construction AI at the end of 2024 with a large and representative sample of nearly 100 companies. Excluded are onsite automated and robotic equipment, covered here in a previous post, and 3D printing, covered here in a 2023 post.

Preconstruction and Cost Estimates

AI is used for site layouts, submittal logs, compliance checks, takeoffs, estimating costs, bids and tenders. Two issues that artificial intelligence (AI) and machine learning (ML) has to address are the lack of standardised industry data and extracting data from different sources, such as PDFs, BIM models and drawings. The first means companies have to build databases and rely on their own projects for data, and there are providers offering assistance with those. These systems use AI and historic data from projects for estimating costs. The second has seen development of AI for image recognition to automate quantity takeoffs from drawings, PDFs and BIM, and scanning drawings to check for missing information and risk assessment.

AITENDERS is a French company that systemises tender and contract management, automates data extraction and analysis.

ALICE TECHNOLOGIES construction planning software uses ML to generate and evaluate thousands of possible construction schedules. This ‘optioneering’ technology simulates different scenarios on a jobsite and provides ‘what if’ analysis to help contractors find the most efficient paths, optimize resource allocation, and minimize project delays. It also streamlines processes like bids and scheduling.

BENTLEY SYSTEMS OpenSite+ uses the iTwin platform for civil site design for residential, commercial and industrial sites, with a copilot and automated drawing for optimising layouts.

BUILDXACT offers cloud-based estimating and job management software that uses AI to create detailed cost estimates, manage budgets, and track expenses. Founded in Australia in 2011, now also in the US, UK, and Canada, the company is focused on residential construction.

CIVILS.AI: extracts construction data from PDFs of contracts, geotech reports, code and compliance documents and uses it for reporting and checking.

CODECOMPLY.AI automatically conducts over 60 different code compliance checks and identifies violations. Checks include fire safety codes, structural regulations, egress and accessibility requirements, and paths of travel.

CONWIZE is a cloud-based cost estimating software with price analysis, bidding automation for subcontractors, tools for managing indirect costs and profit loading, KPIs analysis, risk management capabilities, and predictive analytics.

FIRMUS.AI scans drawing sheets, identifying issues with construction documents, such as incomplete design, scope gaps, missing information, and discrepancies.

mbue have an AI that reads text and automatically reviews architectural drawings to identify changes between drawings.

NOMITECH’s CostOS is an enterprise-scale cost estimating software and BIM integrator, using AI, virtual reality, and Big Data. Does cost and CO2 estimates, and integrates with GIS, CRM and ERP systems. Cost Modeller is a web-based application to store historical cost and CO2 data. Used across construction, mining, oil and gas, utilities and nuclear industries for major projects.

DRAWER AI, an Austin startup, does takeoffs for electrical estimators, who can upload PDF drawings and get quantities of elements such as light fixtures and power devices, with routing based on guidance. It generates a report for use in an estimating system.

IBEAM.AI cloud based, fully automated takeoff software for contractors, subcontractors (covers trades like rebar and concreting, HVAC, plumbing, drywall, roofing etc.) and suppliers.

KREO’s cloud-based takeoff and estimating system uses PDFs or CAD files to produce BQs, estimates and cost plans. It can get measurements from blueprints, and provides choice by combining AI and manual measurement tools.

PINPOINT ANALYTICS have developed a platform for road construction bidding and cost estimates, analysing historical data and adjusting for variables such as materials, labour, equipment, seasonality, geography and market conditions.

RAAP BUILDERS Rooms as a Product, optimization software for prefabricated hotel and multifamily housing projects. Identifies alternate assemblies, industrialized construction methods, and prefabrication options.

SMARTBID for contractors to build a database of prequalified subcontractors, send invitations and share documents, integrates with Autodesk, Procore and ConstructConnect.

THELINK.AI creates a submittal log that lists the materials, products, and documents to be reviewed and approved. Their copilot reads the specifications and creates a log that can be interrogated, updated and shared. Integrates with Procore.

TOGAL AI automates takeoffs and produces estimates, provides cloud based collaboration, has an image search function, and now has a chat tool that allows users to ‘ask’ for reports, specifications and information.

WORKORB, a Canadian startup, automates RFP qualification, response drafting and proposal development, quality checks and contract reviews. The AI can cross reference documents, schedules and addendums and extract compliance obligations and requirements from bids and contracts.

WORKPACK AI for takeoffs using image recognition and text analysis to detect, measure and count relevant objects. It integrates with estimating, project management and progress tracking applications.

Project and Document Management

As well as AI assistants for PM and construction management there are AI systems for workforce and equipment management, claims, code and contract compliance, attendance and access, and risk management. Some PM systems combine project, site and workforce data for planning, scheduling, and task assignments.

AECOM has expertise in gen AI, analytics, ML, data platforms and integration, IoT and telematics. They offer development and integration of a digital strategy for clients, and use AI for project design and management.

ASSIGNAR is a platform that uses AI to optimize workforce and equipment management, with communication, scheduling and time tracking tools. Job assignments include site specifications, safety guidelines, and project orientation in the app, that is also used for quantities, site diaries, timesheets and checklists.

AUTODESK AI provides real-time risk and safety analytics, document management, RFIs, takeoffs, estimates and cost forecasting, bid management, design reviews with clash detection, quality control, tracking, and change order management. BIM 360 IQ scans for safety issues and attaches a tag indicating whether it could lead to a potential fatality. Autodesk partners with other companies like Oracle, Civils.ai, Triax Technologies and SmartBid, and integrates with other applications and systems.

BALFOUR BEATTY is developing an AI assistant, and using AI for safety, and OpenSpace AI for site monitoring and analytics.

BECHTEL began work on an AI assistant in 2018 and established a Big Data and Analytics Centre of Excellence. They are reported to use AI for project planning, risk management and predictive maintenance.

BUILDPASS, an Australian startup, have developed a platform for construction management with an AI toolkit, workflows, plant management, safety, ITPs and quality assurance, and site management tools. Their goal is to become an ‘AI-powered operating system for construction sites’.

CLAIMMASTER.AI is a UK company providing an AI assistant and templates for preparing, tracking and analysing construction claims.

CONSTRUCTABLE.AI a copilot for construction, a platform connecting BIM data, reality capture, and scheduling with AI document search using a chatbot.

CUPIX creates 3D maps and digital twins from 360 degree cameras using AI for progress tracking.

DOCUMENT CRUNCH, an Atlanta startup, analyses and summarises contracts and documents, identifying risks and automating contract compliance.

HOLOBUILDER reality capture uses 360 degree cameras for progress tracking. Allows photos to be attached to floor plans and shared, and manages markup lists.

LARSEN & TOUBRO‘s Smart World offers AI, ML, cloud and integration services. On their own projects AI is used for project planning and construction automation, resource management and risk mitigation.

MICROSOFT Copilot for Project uses Azure and Open AI’s LLM. The new copilot became available in November 2024 and has four capabilities: task plan generation; risk assessments; project status reports; and interactive, chat-like experience. The copilot is an addition to the Dynamics 365 Project Operations platform.

NPLAN developed their own LLM for project forecasting and risk management. It uses ML to analyse historic project data and predict future project outcomes, and creates project schedules, identifies risks, and provides recommendations to avoid potential delays. Their Knowledge Base page is very good, with research papers as well as case studies.

NYFTY AI offers jobsite automation, including communication with subcontractors using text messages and safety inspections. Its system manages attendance and access control, and creates robot assistants (bots) to handle tasks, initiate and record conversations about them. The bots are integrated into Procore and Autodesk.

ORACLE Construction Intelligence Cloud captures, analyses, predicts, and makes recommendations. Their Smart Construction Platform uses project data for schedule, cost, safety, and other performance metrics, and provides collaboration, billing, bidding, payments, and compliance management.

PROCORE has1 million projects, 1 billion construction documents and $1 trillion in construction work on the platform. In June they announced three AI products: Procore Copilot AI with Microsoft Teams is a chatbot for users to ask questions about Procore projects in Teams and receive a summary of information with links to related sources; AI Locations will allow users to scan project drawings and automatically build out project location lists and organize project items with information on RFIs; Procore Maps will be able to filter photos on a map by date to pinpoint specific milestones or events captured during a project timeline.

SKANSKA Sidekick is an internally developed chat bot to for AI-content generation that ‘empowers our teams to summarise information, generate content, and collaborate’. Skanska also uses AI for safety management and project monitoring.

SMARTAPP’s Brena.AI is an assistant developed that automates tasks. generates schedules, automates job reports, updates progress and enhances safety

SMARTBUILD is a platform for contractors with PM, document and resource management, task, safety and financial reports. Uses Microsoft Azure. Has SMART-Sub, a subcontractor construction management version, and SMART-Designer for architects coming soon.

TRIAX TECHNOLOGIES provides safety, labour productivity and equipment tracking solutions using Spot-R video and wearable devices for monitoring.

TRIMBLE has a number of AI offerings. SketchUp Diffusion allows architects and designers to create rendered images based on a natural language text prompt or a preset style. ProjectSight brings automation to project management workflows,

using AI to read and extract critical drawing information for project visualization. Trimble LiveCount uses AI to detect and count symbols on construction drawings.

TRUNK TOOLS workflow automation and document management for administrative tasks using “agents” and text chat to monitor construction schedules and tasks, prepare for meetings, compare project information etc.

Site Monitoring and Safety

Safety systems monitor sites and people using sensors, cameras and wearables like badges and detect hazards. Reality capture and computer vision matches site work to BIM models to track progress and defects, and provide access control, headcounts, timesheets and other analytics.

ACCIONA developed AI-powered platform BIONS for water supply network management in 2020. They have a construction innovation centre and a digital hub for project automation, a HR virtual assistant, and use Boston Dynamics Spot robot with Trimble software.

AI CLEARING uses AI with GIS/CAD integration to optimise construction progress tracking, integrates with Oracle Aconex,

AILYTICS is a Singaporean video analytics company with an AI platform that uses CCTV and video footage to monitor vehicle movements, hazards and site safety, and track progress and productivity. Its face recognition system for workforce tracking would not be accepted in some other countries.

ALWAYSAI computer vision for sites with worker counts, gate and safety monitoring, and progress tracking. Used in nine industries.

BUILDOTS automates progress tracking and predicts delays comparing site scans with project schedules and plans. Its platform identifies discrepancies and suggests adjustments. It ‘offers a single source of truth that fosters efficient collaboration with your supply chain’. Their AI assistant Dot collects information and answers questions using OpenAI’s GPT-4, and integrates with Autodesk’s BIM 360 for tracking and site analytics.

CINTOO, a French startup, have developed a cloud based reality capture platform with BIM workflows, design vs as-built comparisons, and a digital twin platform to virtually navigate project sites.

DRONEDEPLOY uses AI to process images and ML to find patterns.

EVERGUARD AI uses AI to monitor multiple inputs. Its Sentri360 platform integrates computer vision and real-time data from wearables to monitor workers' behaviour and detect hazards.

EYRUS workforce and safety management with registration access control, and video monitoring. Integrates with Autodesk, Procore, Oracle.

GENDA combines workforce management, safety alerts, and logistics in one app, using onsite Bluetooth location beacons for headcounts and task monitoring, and AI based hoist management. Integrates with Procore and Autodesk.

INCON.AI is a Swiss company that provides reality capture for progress tracking. Converts 3D model visualizations into sequenced AR fabrication plans with videos, images, or PDFs, with digital instructions and guidance for installation.

KWANT AI is a workforce management system using smart badges to track access, safety, productivity and compliance. It provides schedules, timesheets, predictive analytics and heatmaps linked to 5D BIM models.

NASKA.AI a cloud-based platform that connects BIM, reality capture, and schedule, automatically comparing a BIM model against the project.

OPENSPACE uses AI for image mapping with 360 degree cameras and photos for documentation and progress tracking. Creates an interactive visual record of construction progress.

SWMS AI creates safety risk assessments using an AI assistant trained on workplace safety data from sources including Safe Work Australia, the Health and Safety Executive, OSHA, and codes of practice. Can be customised to industry or company.

TRACK3D have developed a reality data capture platform for integrating content from drones, 360 degree cameras, laser scanners and mobile devices into a single system to monitor construction progress.

Predictive Maintenance for Construction Equipment

Called telematics, these systems integrate sensors and wireless to collect and record equipment use and performance, and use AI for analysis and predictive maintenance. Typically available as a subscription service, manufacturers now install them on most new equipment and they can be retrofitted to older machines.

CATERPILLAR’s Cat Product Link system for construction machinery. It collects data on hours and fuel use, idle time and location, provides diagnostic codes and predicts maintenance needs.

KOMATSU has its Komtrax system to monitor equipment and predict maintenance. The system collects data on fuel use, productive hours, idle time, load factors, economy vs. power modes, travel times, and for models equipped with load meters, tons, cycles and travel distances.

JOHN DEERE’s JDLink system monitors equipment performance and predicts maintenance. The system provides location, history and utilisation data, alerts and diagnostic reports to help prevent equipment failures and optimize maintenance schedules.

LLUMIN is a software company, not an equipment manufacturer. They provide real-time alerts, automated workflows, analytics and reporting. Used in over a dozen different industries for machine and asset management and maintenance.

VOLVO Construction Equipment’s CareTrack system monitors machine health and predicts maintenance. The system provides data on usage, production and performance.

Design and Planning

One of the first applications of construction AI was in design, which was already software based. Generative design systems generate multiple design options according to specific criteria, by providing alternative solutions using a given set of parameters. Used to optimise a design, examples are crane positioning in site plans, and site and floor plan layouts for office and apartment buildings.

ARCHITECHTURES is a building design platform for optimal residential developments, with quantity takeoffs and parameter presets.

ARKDESIGN creates automated floor plans and feasibility reports for multi-family and mixed-use projects and generate variations based on regulations and building codes.

ARKO.AI is a rendering platform that generates photorealistic 3D models from 2D drawings and sketches, and generates design options. Compatible with Rhino, Revit and Sketchup.

AUGMENTA is an automated building design platform to create designs that are code compliant, error-free and constructible. Also does electrical systems, with plumbing and other coming soon.

BLUEPRINTS AI creates blueprints and generates floorplans and construction drawings using Open AI’s GPT.

GOOGLE EARTH has a design system called Delve that evaluates ‘building and solar design options for early stage urban development’ that can ‘Generate designs in a matter of minutes and evaluate over 80 different performance metrics to uncover the most optimal and sustainable options.’ An explanation of how it works, inputs like energy use and building types, and outputs like gross floor area is here. Use Delve to ‘discover what works best based on financials and metrics like quality-of-life and sustainability, create a Highest and best use study. A Highest and best use study can take 20-30 minutes to generate.’

HYPAR automates the generation of floor plans and turms text into A BUILDING MODEL

PANTHEON AI is an architecture startup aimed at developers, owners and tenants. Their AI can generate floor plans, refine a design and provide construction ready documents.

PLANALOGIC is a design and decision-making platform to find the best performing design to support acquisition decisions, feasibility studies, and scenario analysis.

SKEMA builds a BIM model using a firm’s existing BIM layouts to generate design schemes and construction documents.

SPACEMAKER is an Autodesk platform that does feasibility analysis for architects and urban planners, creates optimal site plans taking into account factors such as sunlight, noise, wind, and regulations, and generates layouts for buildings and spaces.

SWAPP automates dimensioning and tagging of project elements for architects, what they call ‘generative documentation’ with annotations customised for client conventions and standards.

TESTFIT automates generation of building layouts and site plans, optimizing for factors like unit mix, parking, and building efficiency.

Materials

There are AI applications for concrete quality control, and some country-based ones for selection of materials by designers.

AICRETE are developing a quality control operating system for the concrete and aggregates industry integrating with various batch, dispatch, and truck systems.

CAIDIO a Finnish AI company with quality assurance solutions for enhancing the productivity and quality of concrete construction.

GIATEC, a Canadian startup, is developing an AI and IoT sensor enabled platform for the concrete industry, providing real time, wireless concrete temperature and strength measurements and using AI to optimize concrete mixes.

KOJO sources building materials from US preferred vendors, with product availability, pricing, specifications and photos. Integrates with accounting, Autodesk and Procore software. Uses GPT 4 and Hugging Face.

OPUSENSE AI system for real-time concrete strength and temperature monitoring.

STYLIB is a UK material search platform that matches images with suppliers’ products by scanning catalogues.

ZEYKA.AI has 3D design software that helps select materials from a digital library of materials from India's top brands.

Conclusion

This survey divided nearly 100 companies with construction AI systems into six areas: preconstruction and estimating; project and document management; site monitoring and safety; equipment management and maintenance; design and planning; and materials. It is a large and representative sample of the state of play at the end of 2024.

Many of the companies listed are American, which is because that is where AI development is concentrated. There are, however, companies from other countries, such as France, the UK, Switzerland and Finland. Note that any non-English language companies will have been missed.

What is the overall picture this survey of companies offering construction AI at the end of 2024 provides? The number and diversity of point solutions is striking, with all standard tasks and functions addressed by a dozen or more companies. Many of these point solutions automate repetitive tasks for AI for construction firms.

The importance of Autodesk and Procore is apparent from the many systems that integrate with them, and usually with both. These are clearly the dominant industry platforms, and they now have copilots and AI assistants. The other major software companies Trimble, Oracle and Microsoft also have platforms with AI. There are also several new entrants with systems that are comprehensive enough to be called platforms, such as Buildpass and Smartbuild.

Chat GPT was launched in November 2022 by OpenAI, and GPT-4 in March 2023. In two years, AI has gone from being unreliable and error prone to a technology that allows firms to combine and analyse complex and diverse data. It can synthesise, summarise and interpret data, and provide insights and suggestions, however it does not and cannot replace expertise because it also requires supervision and checking of results.

As discussed in Part 1 of this post, construction companies looking at AI have to weigh up four considerations. First is the cost of subscriptions, and whether they have to workload to pay for a platform rather than one or more point solutions. Second is how much difference AI can make to their capability to win, organise and deliver projects. Third is competence in the skills required, and whether their people have or can be trained in these. Fourth is what their competitors are doing, and whether AI can provide a competitive advantage. Cost, capability, competence and competition are the four Cs of construction AI. Firms will have to start working with AI somewhere, sooner rather than later, if they are to survive.

[1] Many of the startups came from Last Week in ConTech, an invaluable source of information on leading edge technology for the industry.

Subscribe on Substack here

https://gerarddevalence.substack.com/

{kind=link}