Data from Australia and the United States

One of the curious things about the construction industry is the perception of it as inefficient and technologically backward, yet it has been at the forefront of many scientific and technical advance for centuries. From Gothic cathedrals to railways and airport terminals, building and construction projects have bought together the best available resources to create increasingly complex structures using the best available technology. Demand for new types of structures with greatly improved capabilities in strength and span drove the development of the modern industry during the first industrial revolution in the nineteenth century. To buildiron-framed and steel-reinforced concrete buildings the industry had to not only master the use of these new materials but also develop the processes and project management skills the new technology required, with the roles of engineers, architects, quantity surveyors, contractors, subcontractors and suppliers becoming defined by the beginning of the twentieth century. The issue then, like today, was not the availability of jobs but the quality of skills during the adoption of new technologies by the industry.

The industry has an undeserved reputation as a technological laggard and for low skilled workers. In reality, the nature of the work attracts people with technical skills who use ‘technological thinking’ to find solutions to the problems a project will encounter between inception and delivery. Technological thinking is essentially problem-solving through trial and error. Regardless of which part of construction they work in, for the vast majority of these people there is a great deal of satisfaction in doing this work well, following relevant codes of practice and meeting the required standards.

This post looks at data on construction employment, qualifications and occupations in the Australian and United States industries. It is not a comparison, because the data is not the same, but an attempt to relate changes in the composition of the workforce to changes in the industry, such as the volume and nature of work and the types of projects. Given the data, this analysis can only be indicative and the conclusions tentative. However, there is good evidence that the industry is neither a technological laggard nor an industry with an unqualified and low skilled workforce, and that these are common misperceptions and misrepresentations of construction.

Australian Construction Employment Trends

Employment in the Australian industry has grown strongly over the last couple of decades, from 664,993 people in November 2000 to 994,283 in November 2010 to 1,363,057 in November 2024 [1], and over that period there has been both stability and change in the composition of the workforce. The percentage share of Technicians and trades has been and is around 50% of the workforce, similarly Labourers have accounted for 16-17% since 2000. During the mining boom the share of Machinery operators and drivers rose to 9% in 2012, but had fallen to 6% by 2024, the lowest share since 2000. As Figure 1 shows, the combined share of these onsite workers rose from 75% in 2000 to 77% in 2012, and was 73% in 2024.

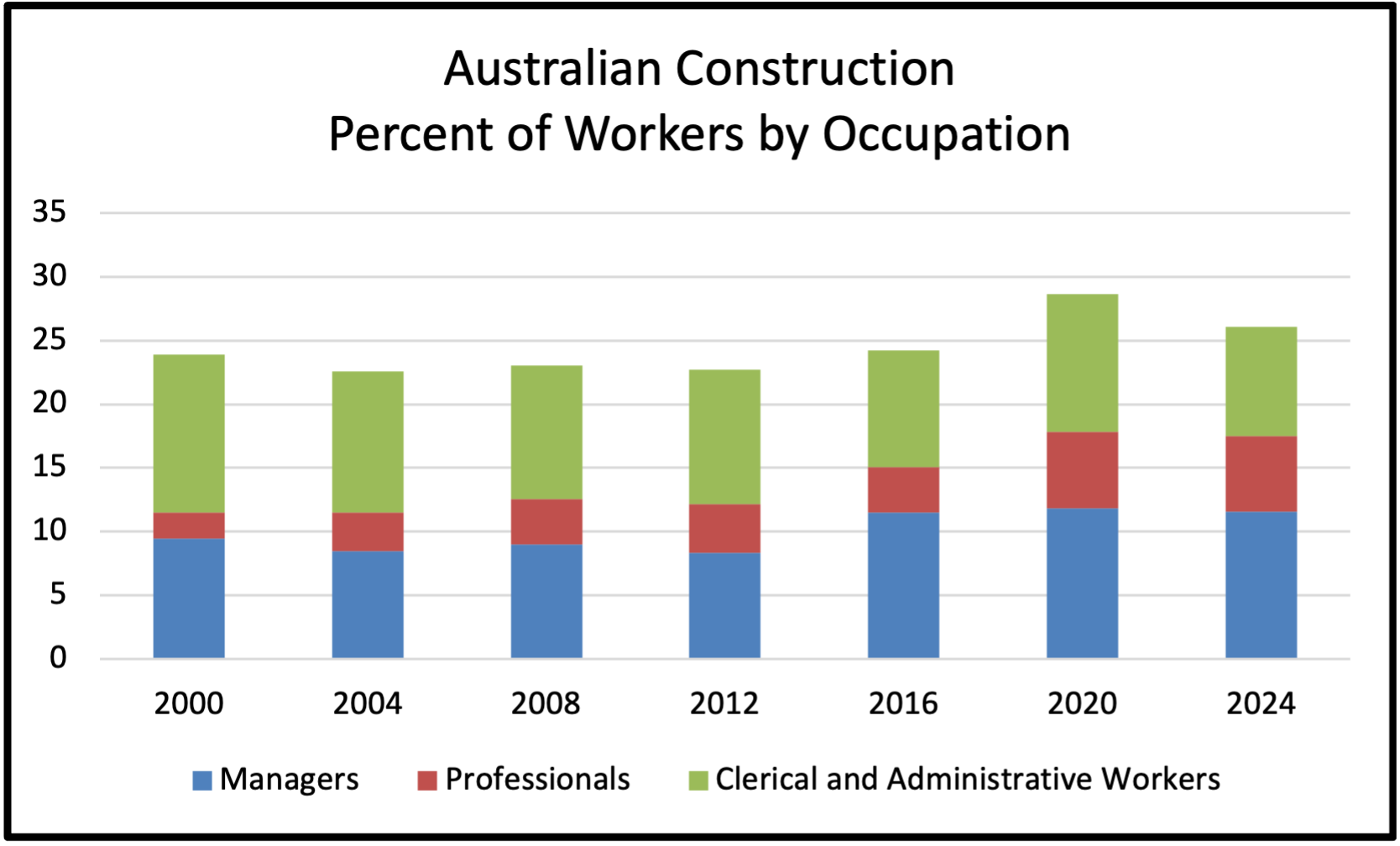

Figure 1. Australian construction workforce composition

Source: ABS 6291 Employed persons by Industry division and Occupation.

It is in the other occupations that the major changes have been happening, and here the trends have been long-running and gradual. The share of Clerical and administrative workers has steadily declined from 12.5% in 2000 to 8.5% in 2024, falling by a third over that time. The share of professionals was 2% in 2000, 4% in 2012 and 6% in 2024. And the share of Managers has increased from 9% in 2000 to 12% in 2016, where it has been since. As Figure 2 shows, the increase in the share of professionals has been the most significant change in workforce composition.

Figure 2. Australian construction workforce composition

Source: ABS 6291 Employed persons by Industry division and Occupation.

Putting the numbers of people employed in different occupations adds some perspective. This data does not go back past 2023 because of the introduction of a revised classification system for occupations, however over the relatively short period between August 2023 and November 2024 there were some significant changes. In particular, the number of Professionals increased from 61,900 to 81,100, a dramatic change, and the number of Community and personal service workers went from 1,100 to 3,200. The number of Managers and labourers also increased, but Clerical and Sales worker numbers both fell, as did the number of Machinery operators.

Table 1. Australian construction, number employed ‘000, by occupation

Source: ABS 6291 Employed persons by Industry division and Occupation.

Finally, another Australian Bureau of Statistics publication has qualifications and work by industry, and table 2 shows that two thirds of construction workers have gained a qualification after leaving school, and 14% have a bachelor degree or higher.

Table 2. Construction workers by level of qualification

Source: ABS Education and Work, May 2024.

The Australian Computer Society’s 2024 Digital Pulse report found Construction employed 12,512 technology workers (in information technology and telecommunications jobs), with 4,983 in management and operations, 2,970 in technical and professional, and 4,559 in ICT trades. That does not include the technology workers employed by the architecture, engineering and project management firms in the Professional, Scientific and technical services industry (possibly 10% of a total of 138,058 outside Computer system design and services).

United States Construction Employment Trends

In the U.S. the data is organised differently, and there are no qualifications by industry data available. There have been significant changes in the composition of the construction workforce, particularly in the last few years. For most years from 2000 to 2009 the Nonproduction employees share of total employment was between 22 and 23%, then from 2009 to mid-2017 it was 24% before rising to 25% at the end of 2017. In 2020 the share rose again to 26% and by 2024 was up to 27.5%. The number of Nonproduction employees in December 2000 was 1,503,000 and almost the same in 2014 at 1,553,000. From 2015 the number began increasing, to 1,903,000 in 2020 and 2,069,000 in 2022, and reached 2,284,000 in 2024 [2].

Figure 3. US construction employment

Source: U.S. Bureau of Labor Statistics, Production and Nonsupervisory Employees, Construction, All Employees, Construction, retrieved from ALFRED, Federal Reserve Bank of St. Louis.

Another series from the U.S. has a similar pattern, for the number of Managers employed in Construction in January. Employment of Managers was 335,000 in 2000 and 414,000 in 2013, before it started increasing and almost doubled, going from 428,000 in 2014 to 785,000 in 2024. Because this was a much larger increase than the increase in Nonproduction employees over that period, the share of Managers in Nonproduction employees went from 22% in 2020 to 26% in 2013 to 32% in 2022, and was 34% in2024 [3].

Figure 4. Number of managers employed in U.S. construction

Source: U.S. Bureau of Labor Statistics, Employed full time: Wage and salary workers: Construction managers occupations: 16 years and over, retrieved from FRED, Federal Reserve Bank of St. Louis.

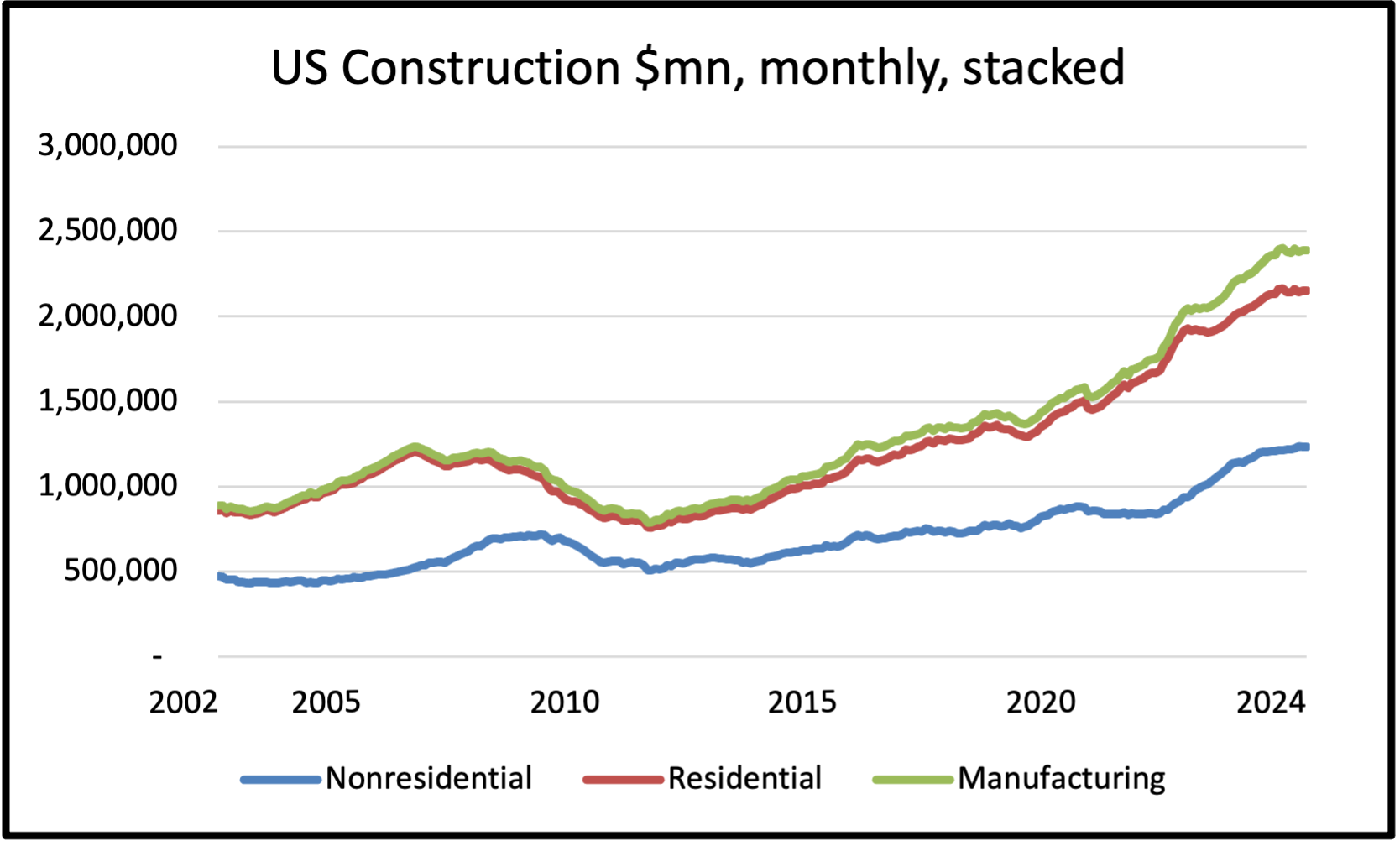

These trends in U.S. construction employment suggest a change in the industry around 2014-15. Total construction spending was recovering from the downturn after the recession in 2008-09, when monthly spending fell below $800 million, and was back to $1 billion in 2014. By 2020 the monthly spend was up to $1.5 billion. By historical standards this was a solid recovery but not exceptional. However, between 2020 and 2024 the total spend went up to $2.15 billion, driven by a doubling of manufacturing construction to $236 million a month as a result of the Biden Administration’s industrial policies that provided subsidies to build semiconductor fabs, data centres, grid infrastructure and renewable energy sites.

With that increase in manufacturing construction, the number of Nonproduction employees and construction Managers also increased. The timing of this cannot be a coincidence, and could be attributed to the complexity and scale of the chip fabs, data centres and other computer and energy projects underway due the subsidies provided by the Biden Administration. Further, the change in employment was a break in the existing trend of gradually increasing employment of Nonproduction employees and construction Managers. The inflection point was 2021.

Figure 5. U.S. total construction spending, seasonally adjusted

Source: U.S. Census Bureau, Total Construction Spending: Total Construction in the United States, retrieved from FRED, Federal Reserve Bank of St. Louis.

The U.S. Bureau Of labour Statistics has detailed occupational data for 2023, but unfortunately this is not available for earlier surveys so a comparison cannot be made. However, the 2023 data is useful because it has the number employed in construction in managerial, supervisory or technical support occupations across the industry divisions of trades, non-residential and residential building, and engineering. These total 1,030,370 people, or 13% of total construction employment in 2023 of 8,120,000, which would the other half of Nonproduction employees that are not cost estimators or doing other clerical and administrative work. Many of these employees can be assumed to have a bachelor degree, for example it is a requirement for construction and architectural managers.

As Table 3 shows, the great majority are employed as trades supervisors (609,580) and construction managers (266,140). The third largest category is architecture and engineering (103,940). The fourth is computer occupations (22,080), and fifth OH&S (19,600). The others are compliance officers (5,660) and architectural managers (3,370).

Table 3. Number employed by occupation and industry division in May 2023

Note 1: The number here of Managers and Supervisors combined is more than the number of Construction Managers in Figure 2 above.

Note 2: Compliance Officers evaluate conformity with laws and regulations governing licenses and permits, and excludes Occupational Health and Safety and Construction and Building Inspectors.

Source: U.S. Bureau Of labour Statistics, Occupational Employment and Wages.

Trades requiring qualifications like equipment operators (321,730), electricians (558,750), plumbers (384,870) and building inspectors (13,550) employed another 1,278,900 people. Adding these trade workers to the 1,030,370 managers and professionals above gives 2,309,270 and 28% of total construction employment in 2023 of 8,120,000. There were another 2,475,690 people employed in construction trades in 2023 as bricklayers, plasterers, painters etc., and many but not all of these workers would also have a certificate or diploma qualification. When the three groups are combined, this is over half the total number of employees. The BLS number of unqualified and unskilled workers was small, there were 858,900 laborers and 174,200 construction trades helpers.

Change Drivers

What can account for these changes in the composition construction employment in Australia and the U.S.? There are three reasons that are widely agreed on. The first is increased regulation, compliance and planning leading to more people spending more time to meet those requirements. In the U.S. there is the National Environmental Policy Act (NEPA), federal environmental legislation requires agencies to produce an environmental impact statement (EIS) before the project can start. These statements can be thousands of pages long and take years to prepare, and NEPA is a frequent target of criticism and reform efforts [4]. Some stats from a Thomas Hochman post on NEPA in December:

- Average environmental impact statement preparation time is 4.2 years as of 2022

- Average review time grew from 3.4 years in 2008 to 4+ years by 2015, increasing by an average of 37 days per year

- Average delay from environmental review publication to resolution of legal challenge: 4.2 years

- Even a "finding of no significant impact" can take extensive time and documentation (1,200+ pages in one case)

- Up to $400 million spent just on regulatory/environmental review process for major projects

- Solar projects: 64% litigation rate

- 72% of NEPA litigation initiated by NGOs

In Australia planning rules are highly prescriptive and complex, with zoning, other regulations, and lengthy development approval processes reducing the ability of housing markets to respond to demand. Research on apartment prices in 2020 and house prices in 2018 by the Reserve bank found planning and zoning restrictions raised prices by up to 70%. A 2021 survey by Infrastructure Australia found: ‘Contractors and investors viewed planning and environmental approval processes as an unpredictable risk to project timelines and a driver of delay. The need to coordinate across multiple layers of government to obtain approvals, and the requirement to meet increasingly onerous conditions attached to many approvals, (e.g. in relation environmental approvals) prompted concern over delivery times’ (p.44).

A second reason is the digitisation of construction and use of BIM leading to increasing offsite employment and project planning. A 2023 Brookings Institute report found only 23% of U.S. jobs were ‘low digitalisation’ in 2020 compared to 52% in 2003. From 2002 to 2010 the share of occupations with a high digitalization level doubled, from 9% to 18%, and in 2020 rose to 26%. A 2021 report by RMIT University found that 87% of jobs in Australia require digital literacy skills, and the 2024 submission by Industry Skills Australia to the Commonwealth Government’s Inquiry into the Digital Transformation of Workplaces (available here with all the other submissions) predicted only 45% of construction jobs would not be impacted by digital technology by 2030.

And a similar argument has increasing offsite manufacturing reducing the number of workers onsite and raising the proportion of offsite workers. The actual extent of the effect is unknown, but is likely to be marginal as the point is not replacing workers but moving them offsite, and there is still substantial site preparation and assembly work involved. Offsite manufacturing also requires detailed digital design and production planning work.

Conclusion

The construction industry is neither a technological laggard nor an industry with an unqualified and low skilled workforce. These are common misperceptions that probably are often the result of people seeing poorly organised and managed sites, which could be addressed through better site facilities and maintenance. In fact, the industry employs a wide range of skills and requires technical competence from the majority of its workers. In Australia, two thirds of the workforce have a post-school qualification, and in the U.S. it is over half. In both countries the share of unskilled labourers is small, at around 10% of the workforce [5].

There are other interesting parallels between Australia and the U.S. In Australia, the share of professionals rose from 2% in 2000 to 6% in 2024, and the share of Managers increased from 9% in 2000 to 12%. Adding the 2024 8% share of Clerical and administrative workers makes 26% in these occupations. In the U.S. between 2014 and 2020 the share of Nonproduction employees rose from 24% to 26%. In both countries the number of Managers has increased by 50%. The share of workers with a bachelors degree or higher is also the same, around 14%.

Why, despite the differences in scale and output mix in the two countries, is the composition of the workforce so similar? To some extent it must be because the methods and processes followed in design, development, construction and project management are similar, as is the use of machinery and equipment. There is not a lot of difference in some types of projects, such as commercial and institutional buildings and road and rail infrastructure. Another factor would be the geographical dispersion of activity, both are large countries and work is spread out across regions.

The trend in both countries is toward fewer low skilled jobs, and this applies to both onsite labourers and offsite clerical and administrative workers. An increasing share of jobs requires qualifications, and more of these workers have university qualifications. This is not to suggest there will be no unskilled workers in future construction, but there is no reason to believe these trends have run their course.

[1] Discussed in a previous post Australian Construction and the Shortage of Workers

[2] Production employees include working supervisors and all nonsupervisory employees engaged in production operations. Nonsupervisory employees includes office and clerical workers, repairers, salespersons, operators, drivers, laborers and other employees at similar occupational levels.

[3] Construction Managers: Plan, direct, or coordinate, usually through subordinate supervisory personnel, activities concerned with the construction and maintenance of structures, facilities, and systems. Participate in the conceptual development of a construction project and oversee its organization, scheduling, budgeting, and implementation. Includes managers in specialized construction fields, such as carpentry or plumbing. From the Bureau Of labour Statistics Standard Occupational Classification.

[4] For a history and how NEPA works see Brian Potter https://www.construction-physics.com/p/how-nepa-works. For a survey of research see Noah Smith https://www.noahpinion.blog/p/the-big-nepa-roundup. For comprehensive data see Thomas Hochman https://www.greentape.pub/p/nepastats and why reform is necessary https://www.greentape.pub/p/revisiting-pro-nepa-studies

[5] The review of the UK's ITBs by Mark Farmer has just been released. It was done in 2023 and the data is for 2020, but it says on page 41:

"In terms of the job role make up of the construction industry, 57% are elementary level, plant or trade craft operatives. Professional, management and technical roles constitute 33% of the workforce with 10% of the workforce are in support or administrative roles.

In terms of attainment, 73% of the workforce are at level 3 and below, including 5% who are unqualified. 21% are degree level or above qualified."

Interesting because similar to Australia and the US.

https://www.gov.uk/government/publications/2023-industry-training-board-itb-review

Subscribe on Substack here

https://gerarddevalence.substack.com/