How significant for housing supply are loans to investors for new construction?

Negative gearing is a tax policy that allows property investors to offset losses from rental properties against taxable income. Its effect on housing supply and affordability is controversial, with some arguing negative gearing encourages investment in rental properties and increases housing supply, while others argue most of that investment goes into existing properties, so negative gearing increases demand for rental properties and drives up prices, making it more expensive for first-home buyers. However, the effect of negatively geared investor loans on housing supply is not as clear as the effect on house prices. There is nothing in negative gearing to specifically act as an incentive for construction of new homes, but that does not mean it does not increase the supply of housing.

The Australian Taxation Office definition of negative gearing is: ‘A rental property is negatively geared if it is purchased with borrowed funds and the net rental income, after deducting expenses, is less than the interest on the loan.’ With a negatively geared property the taxpayer makes a loss, but that loss is tax-deductible against other income, including ordinary wages and salaries, and thus other taxpayers help the property investor meet the costs. investors know rental returns are less than operating and interest costs but they expect property values will increase so losses will be more than covered by capital gains when the property is sold. The higher the income of the taxpayer the more favourable this type of gearing becomes.

Two examples of arguments for increased supply are reports for the Property Council in 2014 and 2019. The 2014 report by ACIL Allen claimed around a third of all loans for new dwelling construction were to investors and it was a myth that negative gearing does nothing to support housing supply. The later 2019 report by Deloitte Access Economics found limiting negative gearing to new housing and reducing the Capital Gains Tax (CGT) discount from 50% to 25% would lead to a decline in prices for new property of 3.6% by 2030 that ‘in turn results in a decline in dwelling commencements which is estimated to be 4.1% below baseline in 2030. The decline in commencements each year reduces the stock of dwellings over time … The stock of dwellings is estimated to be 0.4% lower by 2030.’

This post addresses the question of the significance of negative gearing for supply of new housing. It starts by looking at the data available from the Australian Bureau of Statistics on lending to investors, then compares the data on loans to investors for new construction to the building approvals data, and finally the Australian Tax Office data on deductions for rental properties is considered.

Lending For Dwellings

Australian Bureau of Statistics’ Lending Finance data shows over half of the value of new lending is to investors, and ABS census data shows nearly a third of existing properties are owned by investors. How significant for supply of new housing are loans to investors for new construction?

Although a lot of lending for dwellings goes to owner occupiers in Australia, since 2019 the share of lending to investors for dwellings has been increasing. This went from 29% to 38% for the number of dwellings and from 39% to 60% for the value, in Figure 1. While these are the headline numbers often used when discussing negative gearing, they are not relevant to the supply of new housing because the great majority of this lending to investors is for established housing, not new construction.

Figure1. Investor share of total lending for dwellings

Source: ABS 5601.

Between 2019 and 2024 the shares of lending to investors changed, as the proportion of investor loans for new construction increased from around 11% to 14.5% of the number of dwellings and from about 10% to 14% of the value, while lending for newly built dwellings more than halved over the period, from around 11% to under 5%. As a result, their combined share for new dwellings of total investor lending has fallen from 22% to 19%, which is not insignificant. As Figure 2 shows, over the last two years the growth of lending for existing dwellings has been much faster than lending for new construction.

Figure 2. Lending to investors for dwellings

Source: ABS 5601. These ABS data series begin in September 2019.

For housing supply the investor loan share for construction new dwellings of total lending is the important point, and that share is only 6% of the number and 8% of the value, in Figure 3. That share is very low because so much more lending goes into existing properties. However, although this suggests investor loans play a marginal role in the supply of new housing, and not all investors are negatively geared, this is not the whole story.

Figure 3. Lending to investors for construction of new dwellings

Source: ABS 5601. These ABS data series begin in September 2019.

Building Approvals

Comparing the number and value of investor loans for new construction of dwellings to building approvals shows the role of investors in housing supply has become more important over the last few years. In 2019 the shares of investor loans for new construction were 8% of the number of private sector building approvals for dwellings and 10% of the value, but in 2024 they had increased to 16% and 21% of the number and value respectively, in Figures 4 and 5. These are more significant shares than those in the lending data.

Figure 4. Investor loans for new construction and number of building approvals

Source: ABS 8731 and 5601.

The increase in the investor share of building approvals is a combination of a decline in approvals since 2021, which can be attributed to the 30-40% increase in costs since then, and the increase in investor loans noted above. The increase in the share of the value of both investor loans for new construction and the share of building approvals suggest this is funding for houses rather than apartments or medium density development.

Figure 5. Investor loans for new construction and value of building approvals

Source: ABS 8731 and 5601.

The 16% investor share of the number of dwellings approved is significant. There are, however, two caveats to this. The first is that not all approvals become commencements, although most do eventually get started. The second is that not all investor loans are negatively geared.

Australian Tax Office Data

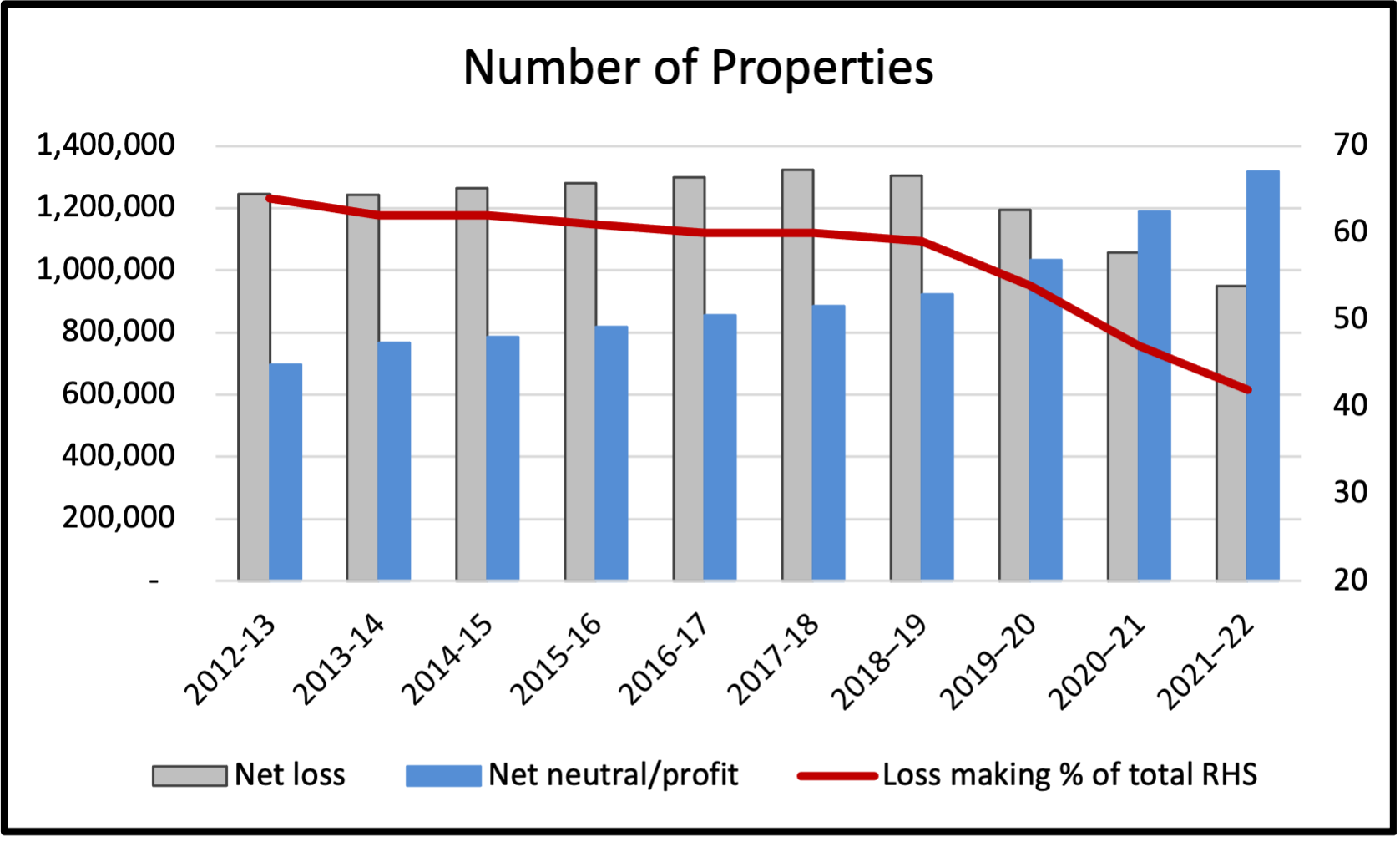

The most recent ATO statistics are for the 2021-2022 financial year because of the time taken to submit and process returns, so there is no data for the last two years. The share of investors who are negatively geared rises and falls with changes in interest rates. During the financial crisis in 2008 when the cash rate was 7.25% the share of negatively geared rental properties was over 69%. As Figure 6 shows, in the years before before 2019-20 total net rental income was negative, but as the cash rate fell to 0.1% in 2020 total deductions also decreased and the share of negatively geared rental properties fell below 50%. Table 1 has the same data going back a few more years to 2014-15.

Figure 6. Total rental income and deductions

Table 1. Total rental income and deductions, $ billion

In the ATO data going back to 1999-2000 the majority of investors have been negatively geared, and since 2002 it has been between 60% and 70%. As Figure 7 shows around 60% of rental properties were negatively geared in the six years before 2019-20. Because interest rates were at record lows in 2020-21 and 2021-22 the number of negatively geared properties fell to 47% and 42%. With the increase in the cash rate after 2022 to 4.35% in 2024 the share of negatively geared properties should be trending upward to the long-run level of over 60%.

Figure 7. Number of rental properties by rental outcome

Source: ATO Taxation Statistics

What is not in the data from either the ATO or the ABS is the share of negatively geared investor loans for new construction, the question this post is addressing. The assumption can be made that the share is the same 60 to 70% for new builds as for negatively geared existing properties, but there is no way of knowing if that is the case. In all likelihood it is less, possibly much less, because investing in a new build would be seen by the typical negatively geared investor, who has one property, as more risky than an existing dwelling. The ATO data has 70% of investors with one property.

Of the investor loan share of 16% of the number of building approvals, if around a third are negatively geared then the 16% becomes 5 or 6% of building approvals, if it were half then 8% of the number of approvals would be negatively geared. Even at the high range assumption of two thirds of investor loans for new construction being negatively geared, that is barely more than 10% of approvals.

Conclusion

Negative gearing is a tax incentive that allows investors to deduct rental property losses from other income. Australian Bureau of Statistics’ Lending Finance figures show about 85% of investment in rental properties is for purchase of existing properties, not building new ones. Because it increases demand for rental properties, this drives up prices for existing properties, making it more expensive for first-home buyers. However, the effect of negatively geared investor loans on housing supply is not as clear as the effect on house prices. There is nothing in negative gearing to specifically act as an incentive for construction of new homes, but that does not mean it does not increase the supply of housing.

Between 2019 and 2024 the share of lending going to investors for dwellings went from 29% to 38% for the number of dwellings and from 39% to 60% for the value, The great majority of this lending is for established housing, not new construction. The proportion of investor loans for new construction increased from around 11% to 14.5% of the number of dwellings and from about 10% to 14% of the value, while lending for newly built dwellings fell from 11% to under 5%. For housing supply, the investor loan share for construction new dwellings of total lending is only 6% of the number and 8% of the value. The higher share of the value of investor loans for new construction and suggests this is funding for houses rather than apartments.

The role of investors in housing supply has become more important. In 2019 investor loans for new construction were 8% of the number of private sector building approvals for dwellings and 10% of the value, but by 2024 had increased to 16% and 21% of the number and value respectively. That 16% share of the number of dwellings approved is significant, but not all approvals become commencements, although most do eventually get started, and not all investor loans are negatively geared. This rise in the investor share of building approvals is due to the combination of a decline in approvals since 2021 and the increase in investor loans.

Australian Tax Office data going back to 1999-2000 shows the majority of rental properties have been negatively geared, with between 60% and 70% negatively geared before 2019-20. Because interest rates were reduced to 0.1% in 2020-21 and 2021-22, negatively geared investors fell to 42% of properties. With the increase in interest rates after 2022 the share should be trending back toward the long-run level of 60% or more.

The data from the ATO and the ABS does not give the share of negatively geared investor loans for new construction, the question this post addresses. An assumption has to be made. Is the share the same 60 to 70% for new builds as for existing properties? Probably less, possibly much less, because investing in a new build would be seen by the typical negatively geared investor, who has one property, as more risky than an existing dwelling. Of the investor loan share of 16% of the number of building approvals, if around a third are negatively geared then the 16% becomes 5 to 6% of building approvals, if it were half then 8% or at two thirds slightly over 10% of the number of approvals would be negatively geared.

At between 5 and 10% of building approvals for new dwellings, negatively geared investor loans do not play an important role in the supply of new dwellings, and they are more likely to be for houses than apartments. To increase supply better targeted policies are needed and would be more effective.