The level of technical efficiency of an industry is determined by the technology used in the production process, which is embodied in the machinery, equipment, software and devices available to producers. The most efficient firms in an industry are on or close to the efficiency frontier, and typically there is a distribution of firms within an industry with some small firms having the lowest level of efficiency. Although some firms are on the efficiency frontier, many firms are inside the frontier (i.e. are less efficient), and the level of industry productivity will be around the average level of all firms. Construction fits this picture.

This post first looks at recent research on productivity measurement issues, which finds their well-known problems are not a satisfactory explanation for the lack of growth in construction productivity. Then recent research using Data envelopment analysis (DEA) is reviewed, an econometric method used to measure the efficiency of firms and industries. Construction is found to be at a high level of technical efficiency and close to the limits of current technology. Therefore, to increase construction productivity new technology will be required.

Productivity and Real Output

Productivity is determined by the amount of machinery and equipment used (physical capital) and the level of skills and training of employees (human capital). Over time, as firms and industries replace old machinery and equipment with new, upgraded versions, productivity is expected to increase. The mystery of construction productivity is why there has been no increase in productivity, despite the improvements in human and physical capital, since the first attempts to measure it in the 1960s (in the US).

Measurement problems and data issues are the most widely accepted reasons for the lack of construction productivity growth, the construction deflator may underestimate industry output thus lowering the level of measured productivity. However, recent research has found these measurement issues cannot fully account for the lack of productivity growth. The problem is real and another explanation is necessary, with results from a different branch of productivity research suggesting that explanation may be a high level of technical efficiency.

The accepted reason for the low rate of construction productivity growth is the underestimation of real output, measured as value added (the total value of goods and services produced after deducting the costs in the production process and adjusting for movements in prices). The construction deflator may not fully take improved quality and relevant input price movements into account, leading to underestimation of real value added. Recent American research has investigated this issue.

Addressing the problem of measuring real output in an industry as diverse as construction, Sveikauskas and colleagues at the US Bureau of Labour Statistics published estimated real construction value added per hour worked in four construction sub-industries, using four specific deflators and including subcontractor hours. Between 2007 and 2020 productivity fell in single-family residential and multiple-family housing construction, but rose in industrial and highway, street, and bridge construction, following a rising volume of work in the latter two sub-industries. Overall productivity for the four sub-industries was flat because these rises and falls balanced out.

Garcia and Molloy asked ‘Can Measurement Error Explain Slow Productivity Growth in Construction?’. Their answer was no, ‘we estimate that productivity was essentially flat in the construction sector from 1987 to 2019,’ although it was not as low as implied by official statistics when they adjusted for the improved quality of houses. Their analysis found a small upward bias in deflators related to unobserved improvements in structure quality, ‘but the magnitude is not large enough to alter the view that construction-sector productivity growth has been weak. We also find only small contributions from other potential sources of measurement error.’ The implication of this research is that a small increase in productivity has been absorbed by higher but unobserved (i.e. not in the data) quality, therefore no growth in measured construction productivity.

Another recent significant contribution came in a paper from Goolsbee and Syverson with the arresting title ‘The Strange and Awful Path of Productivity in the U.S. Construction Sector”’. The time period is 1950 to 2019. They focus on measurement problems as an explanation of poor performance: ‘we update some of this previous work and extend it to some new data sources and hypotheses. Together, these new approaches seem to reinforce the view that the poor performance is not just a figment of measurement error.’

Their paper concludes, however, that measurement error is ‘probably not the sole source of the stagnation’, i.e. the statistics may have some issues, but the problem is real. Construction productivity, despite the obvious improvements in materials, tools and techniques over the last few decades, has not increased. And this is not unique to the US, for countries around the world, the same result has been found. It is a universal problem.

Technical Efficiency

Technical efficiency is defined as the ability of firms and industries to produce as much output as possible, given the inputs of labour and capital used and the level of technology available. At maximum efficiency, to increase output requires adding another input to the system of production, such as an extra worker or another machine.

Data envelopment analysis (DEA) estimates efficiency by measuring the ratio of total inputs employed to total output produced for each member of a group. This ratio is then compared to the others in the sample group of firms, industries or countries to estimate relative efficiency. DEA identifies the most efficient provider of a good or service by the ability to produce a given level of output using the least number of inputs, then measures relative efficiency against that benchmark for the sample group.

With DEA it is important that the level of technology used is similar across the firms or industries in any comparison. In construction, firms have access to current technology, in the form of materials, components and equipment, and the organization of production is based on high level of standardization of parts and processes. With a few exceptions for specialised work (tunnels etc.), the technology available to and used by firms does not vary much from firm to firm.

DEA has been used to assess productivity and efficiency levels in many industries. DEA was first applied to the construction industry in Hong Kong in the late 1990s, and over the last few years there have been DEA papers on construction in Spain, Sweden, Europe, Hong Kong, China, New Zealand and Australia. This research broadly found construction productivity has slowly increased over time, but it is pro-cyclical and follows rises and falls in the volume of work. There are two other common findings. The first is not surprising, larger firms are more efficient than small ones and there is a significant within-industry difference between the best and worst firms. The second, however, is not so obvious.

These DEA studies find the overall level of technical efficiency in construction is high, and for the best firms very high. This may not be something many people dealing with the day-to-day information and coordination problems in construction would agree with but, using DEA and industry level data, that is what this research finds. And like productivity, technical efficiency is strongly pro-cyclical, rising and falling as the volume of work increases and falls. Periods of full technical efficiency coincide with periods of the strongest productivity growth.

The industry in all the countries where construction has been analysed with DEA is efficient, based on the econometric instrument of DEA and data on the volume of work, industry value added, capital stock and employment. Full technical efficiency is the complete use of all available inputs of capital and labour in the production of output and value added, or to put it another way, there is a point where the industry is at maximum capacity and there are no underutilised inputs. At that point on the efficiency frontier more input is required to increase output, such as an extra worker or machine.

This can go a long way as an explanation of the productivity problem. When the level of work is high and increasing, productivity improves until the industry is approaching the efficiency frontier, where more workers are needed to increase output. Therefore productivity stops growing. As the volume of work falls during the contraction phase of the building cycle and firms retain workers in the expectation of future work, so the level of industry productivity falls, ending up where it started.

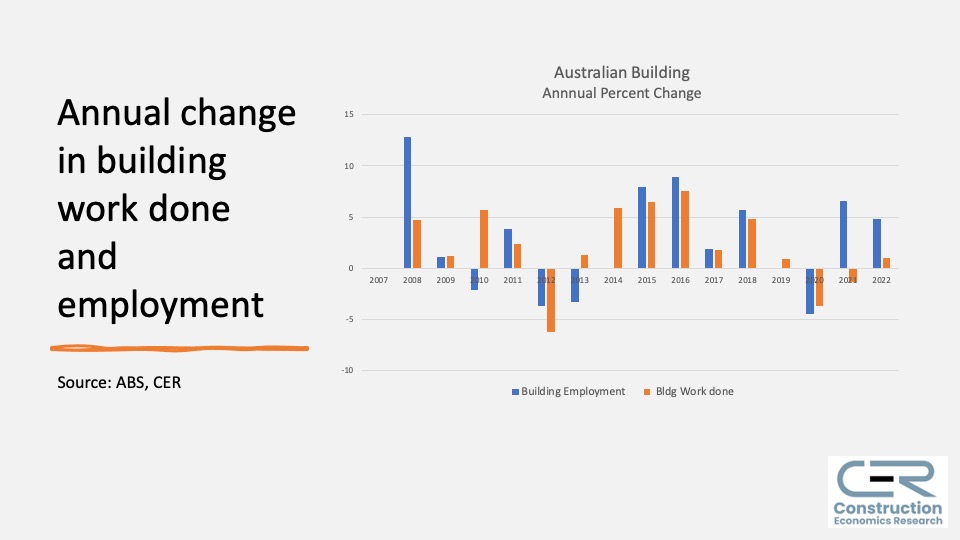

The Australian construction industry illustrates this pattern. Between 2007 and 2022 the volume of construction work done increased by 29 percent, and construction employment by 26 percent. This similarity in the changes over time indicates that, over this period, the industry has turned inputs into buildings and structures using current production technology (machinery, materials, management etc.) at a high level of technical efficiency. It also identifies the strong relationship between an increase in work done (output) and employment, which will also increase. In construction, an increase in output requires more workers, over time productivity as output per worker doesn’t change.

Figure 1. Three measures of productivity

Between 2007 and 2022 the industry went through a long cycle as the volume of work done first rose by 50 percent, peaking in 2013, but then contracted by 23 percent between 2013 and 2022. There was a significant increase in work done per person employed due to the large amount of machinery and equipment required during the engineering construction boom of 2011-14 (e.g. offshore oil rigs and LNG plants). Industry gross value added (broadly the difference between revenue and expenses) per person did not increase as much because that machinery and equipment was purchased as an intermediate input to construction from other industries, resulting in a short-lived, pro-cyclical increase in construction productivity, which ended up where it began.

Conclusion: Why efficiency beats productivity in construction

Despite the efforts made by governments, industry organisations and firms over the past decades, there has been no growth in construction productivity. The rate of growth of productivity of the construction industry has been poor since the 1960s, even by comparison with a long-run overall industry average around two percent a year.

Construction is a labour intensive industry in comparison with manufacturing, with which it is often unfairly compared, but there has been a significant increase in the offsite component of construction, and construction methods have become more capital intensive as the performance of machinery, equipment and tools used has improved. However, the expected productivity growth has not occurred, according to the data from national statistical agencies.

This is the mystery of construction productivity: why there has there been no increase in labour productivity, despite the improvements in human and physical capital, since the first attempts to measure it in the 1960s? Measurement issues leading to underestimation of output are widely believed to be the main problem, however this is not the case, although there may be some underestimation the lack of growth in construction productivity is real. Another explanation is required, and the high level of technical efficiency in construction is suggested.

This post first looked at recent research on productivity measurement issues, which finds their well-known problems are not a satisfactory explanation for the lack of growth in construction productivity. Then recent international research using Data envelopment analysis (DEA) is reviewed, an econometric method used to measure the efficiency of firms and industries, defined as the ability of firms and industries to produce as much output as possible, given the inputs of labour and capital used and the level of technology available.

There is a relationship between the technical efficiency and productivity. The same inputs of labour and capital are used, but efficiency is the quantity of output given inputs while productivity is the ratio of output and those inputs. Labour productivity, for example, is the number or value of units produced divided by the number of hours worked or the number of people employed. The DEA studies find the overall level of technical efficiency in construction is high, and for the best firms very high, and is strongly pro-cyclical, rising and falling as the volume of work increases and falls with high levels of technical efficiency and productivity growth at the peak of the cycle.

The level of technical efficiency is determined by the use of the capital stock available to workers. As the level of capital per worker (machines, software etc.) increases so does output per worker, but as the level of output per worker increases it approaches the limits of the technology currently used in production and, at a high level of technical efficiency, productivity growth is no longer possible.

If productivity growth is no longer possible with the technology currently used in the system of production, which in construction has been developing for well over one hundred years, industry will focus on efficiency and getting the most out of the labour and capital available. Efficiency trumps productivity in construction.